Unlocking Your Retirement Funds: How New NY State Tax Rules Are Reshaping 401(k) Withdrawals

Unlocking Your Retirement Funds: How New NY State Tax Rules Are Reshaping 401(k) Withdrawals

As millions plan for retirement, New York’s evolving stance on 401(k) taxation is turning attention to a critical question: What happens when you draw down your retirement savings? Newer state rules are shifting how NY residents face state income taxes on their 401(k) withdrawals—changes that can significantly impact take-home pay. Unlike federal-only calculations, New York’s progressive tax system adds layers of complexity, making it essential to understand not just federal withholding, but how the state now taxes these post-retirement distributions.

With recent reforms and clear deadlines emerging, retirees must navigate a landscape where procrastination or misunderstanding can cost thousands. Historically, federal taxes governed 401(k) withdrawals, but New York now imposes its own layer of taxation—making effective retirement income planning more urgent than ever. Under current law, legitimate withdrawals from New York-qualified 401(k) plans trigger state tax liability alongside federal withholding.

The state treats these distributions as taxable income, with rates varying depending on total earned income and filing status. For married filers in the highest brackets, this means state taxes can push effective withdrawal rates into the 10–13% range—substantially higher than a flat federal rate.

Understanding New York’s approach begins with recognizing that 401(k) funds are not tax-free even if pre-tax contributions dominate.

Once withdrawn, every dollar becomes taxable at both the state and federal levels. “Retirees often assume 401(k) withdrawals are fully shielded from state taxes,” says Sean Callahan, a tax attorney specializing in retirement planning in Albany. “That’s not true in New York.

The state now expects contributions to be fully accounted for, and the time value of money means even small miscalculations compound over decades.”

Federal vs. State Tax Dynamics: What Retirees Need to Know

- Federal Withholding: Standard withholding on 401(k) distributions reflects IRS guidelines and current tax brackets, with rates depending on W-4 elections and total income.

- New York State Withholding: A separate, mandatory state withholding amount is applied based on projected total income, including federal, Social Security, and other retirement earnings.

- Net Impact: Together, federal and state withholdings determine the immediate cash left after a withdrawal—factors this can affect monthly budgeting, especially in early retirement.

- Filing Status Matters: Single filers, married couples, and those claiming dependents face distinct thresholds and rates set annually by the New York State Department of Taxation and Finance (NYSDTF).

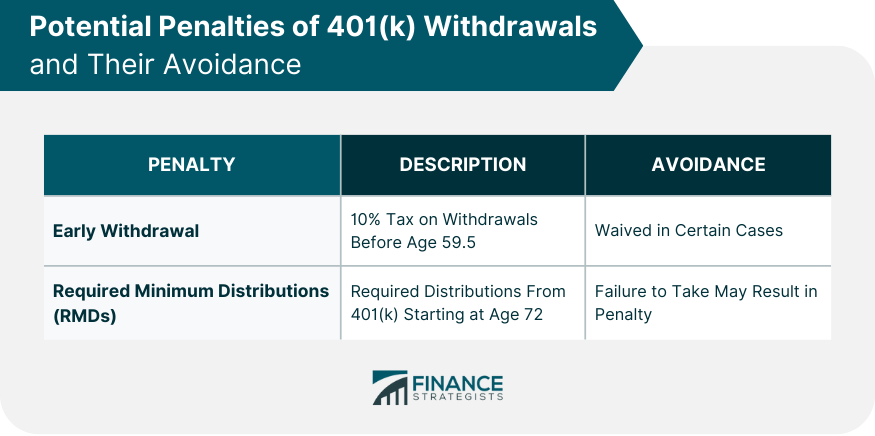

Key Changes: The 2024 Thresholds and New Reporting Requirements

In 2024, New York strengthened its 401(k) tax enforcement with tighter reporting rules and higher effective rates for high-income retirees. Under NYSDTF guidelines, individuals earning over $600,000 face a combined effective tax margin of approximately 14–15% on distributions—rising to nearly 19% for those above $1 million in total retirement income. New filers must now submit updated Schedule EV annually, detailing IRA and 401(k) balances from the prior year, increasing transparency but also administrative burden.

The state applies a tiered withholding schedule: first, withholding mirrors federal withholding for the first portion of withdrawals; beyond that, state taxes apply at progressive rates.

For example, a single filer drawing $60,000 in annual 401(k) distributions may face 4.83% federal withholding and 5.75% New York state withholding—totaling 10.58% before any retirement account exclusions or strategic withdrawals.

Strategic Washouts and Tax Timing: Smarter Withdrawals Reduce Liability

Many retirees overlook a powerful but underused tool: strategic asset sequencing to minimize tax exposure. By staggering 401(k) withdrawals across years, considering other income sources, and potentially converting traditional accounts to Roth over time, savers can smooth taxable income and avoid pushing themselves into higher New York brackets. “Retirees who ignore tax timing often lose 10–15% in real purchasing power,” warns tax advisor Callahan.“A well-planned withdrawal schedule aligns with low-income years, tax credits, or insurance benefits to keep total liabilities in check.”

Specific Requirements for 2024 Withdrawals: Reporting and Exemptions

- Mandatory Reporting: All 401(k) distributors must file NY Form IT-203 by Jan. 31, detailing total deductions, employee contributions, and federal withholding.

- Exemptions:** Non-taxable intersectional assets—such as Social Security benefits not returning to pre-tax dollars—may qualify for full exemption, but requires careful documentation.

- Penalties for Non-Compliance: Filing late or underpaying state taxes on distributions may trigger interest, late fees, or even audits. Proactive filing and accurate reporting protect both funds and credit.

The shift toward aggressive tax awareness in retirement planning is not a temporary trend but a permanent structural change.

Self-employed individuals, those with solo 401(k)s, and traditional plan holders alike now face real financial consequences from delayed or inaccurate tax calculations. Staying informed isn’t optional—it’s a core component of preserving retirement wealth. As state tax codes grow more intricate, knowledge transforms uncertainty into control.

For every dollar withdrawn, California, Texas, or New York taxes may apply—and in New York, those deductions hit hard. Recognizing this dynamic empowers retirees to move with precision, ensuring their savings fulfill their intended purpose: secure, sustainable retirement.

Related Post

Hobbs NM Population: Decoding Every Cyber Battleground with Precision Metrics

JC Monahan Nbc Boston Bio Wiki Age Husband Illness Salary and Net Worth

How Many Sticks of Butter Is 1/2 Cup? The Simple Math Behind Every Kitchen Measure