NatWest Base Rate: A Historical Overview That Shaped British Banking

NatWest Base Rate: A Historical Overview That Shaped British Banking

From its quiet inception in the post-war era to its current role as a cornerstone of India’s—and increasingly the UK’s—banking transparency, the NatWest Base Rate reflects decades of economic transformation, regulatory evolution, and shifting monetary policy. This persistent benchmark, once a hidden mechanism behind lending costs, now stands as a public-facing indicator of interest rate trends across the nation’s financial landscape. Its journey through over 70 years reveals not just technical changes, but also the broader narrative of how central banking adapts to national and global challenges.

The NatWest Base Rate—officially known as the bank’s border rate or simply the base rate—serves as the starting point for variable-rate lending and savings products across British banks. First formalized in the early 1970s, it emerged during a period when financial institutions began formalizing benchmark rates to reflect changing economic conditions. “Rates are no longer arbitrary,” one former NatWest monetary policy advisor noted years ago.

“They reflect real economic forces shaped by inflation, growth, and global events.” This shift from opaque pricing models to transparent benchmarks laid the foundation for greater accountability in banking.

The Birth of Transparency: The Early Years (1970s–1990s)

When the NatWest base rate was first publicly disclosed in the early 1970s, it marked a pivotal moment in British banking history. Prior to this, lending rates were often contractual specifics, shielded from public scrutiny.The introduction of a published rate introduced clarity and comparability. - In 1972, the base rate stood at approximately 8–9%, a figure influenced heavily by post-Bretton Woods volatility. - By the late 1970s, rates rose sharply in tandem with inflation, peaking near 17% by 1979—a sobering reflection of the economic turbulence of the era.

- Throughout the 1980s and 1990s, the base rate remained a sensitive indicator of monetary tightening and easing, responding to Thatcher-era deregulation, high unemployment, and fluctuating oil prices. “The base rate began as a modest tool for internal benchmarking but evolved into a public signal of economic health,” explained a senior Bank of England economist in a 2018 analysis. “Its gradual visibility helped customers and businesses align financial decisions with macroeconomic realities.”

The Modern Era: Integration with Monetary Policy (2000s–2010s)

The early 2000s brought structural changes that deepened the base rate’s significance.As inflation targeting became the Bank of England’s core mandate, the base rate evolved from a reactive gauge into a strategic instrument of monetary policy. - By 2005, the rate hovered around 4.25%, a stable level that supported moderate growth. - The 2008 financial crisis triggered an unprecedented shift: the base rate plummeted to 2.5% by early 2009, among the lowest levels in a generation, as the Bank of England injected liquidity.

- During the Eurozone debt crisis and global recovery phases, the rate cycled between 0.3% and 5.25% as policymakers balanced growth and inflation risks. “The base rate became more than a number—it embodied central bank communication,” noted a NatWest finance editor in a 2016 report. “When rates fell, markets listened; when they rose, confidence wavered.” This period saw the base rate interact closely with quantitative easing and fiscal stimulus, illustrating how banking benchmarks now operate in tandem with broader economic governance.

Navigating Inflation: The Base Rate in the 2020s

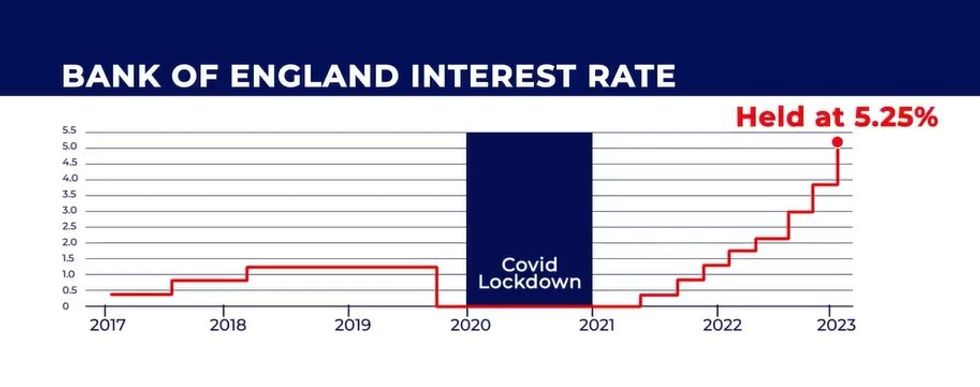

The 2020s have tested the base rate like never before. The pandemic, supply chain disruptions, and energy shocks coalesced into a hyper-inflationary environment, driving the Bank of England’s base rate to a 15-year high of 5.25% by late 2023. - In 2022, the rate surged from near zero to over 4% within 18 months—an aggressive tightening cycle aimed at curbing demand and stabilizing prices.- The base rate now fluctuates in daily market expectations, closely watched by investors and households alike. - By late 2023, with inflation cooling but still above target, the rate remained elevated, signaling cautious optimism and persistent vigilance. “This decade’s base rate journey reflects a world in flux,” said a current Royal Bank of Scotland economist.

“Rates are no longer just about lending—they’re about anchoring trust in a volatile global economy.” The base rate has thus transitioned from a quiet internal reference to a central narrative in public and policy discourse.

Key Milestones and Figures in the Base Rate Timeline

- 1972: First formal publication under NatWest, reflecting growing transparency needs. - 1979: Rate reaches peak of ~17% during high inflation period.- 2009: Base rate cuts to 2.5% amid global financial crisis. - 2019: Rate stabilizes between 0.25% and 0.5%, among the lowest in decades. - 2022–2023: Rapid escalation to 5.25%, the highest since the early 1980s.

Each shift marks not only a monetary adjustment, but a broader recalibration of economic expectations and banking behavior.

The Base Rate Today: A Beacon of Accountability

Today, the NatWest Base Rate functions as both a practical financial benchmark and a public symbol of central bank accountability. With interest rates influencing mortgages, savings, and business loans, the rate’s daily movements ripple through personal finances, pensions, and investment strategies.Transparency—once a novelty—has become a standard, driven in large part by decades of NatWest’s and the Bank of England’s evolving disclosure practices. “The base rate is now woven into the fabric of economic life,” observes a financial journalist with deep coverage of UK banking trends. “It once hid behind contracts; now, it speaks directly to millions, turning complex policy into accessible truth.” This transformation underscores a broader shift: from opaque banking practices to an era of public access, trust, and engagement.

As economic cycles continue to evolve under pressure from climate risk, technological disruption, and global uncertainty, the NatWest Base Rate remains a vital indicator. It stands not just as a number on a spreadsheet, but as a living testament to the resilience, adaptability, and responsibility of British banking.

Related Post

Is Miami MD A Hoax? Separating Fact from Fiction in the FL State Gambit

Did Heather Locklear’s Scandalous Photos Derail Her Hollywood Reign? A Hollywood Fall From Grace

Movierulz Web Series: A Comprehensive Guide to Streaming Today’s Most Addictive Digital Entertainment